India and China’s recent crack down on black money has sent shock waves across the world.

India and China’s recent crack down on black money has sent shock waves across the world.

With illicit money stocked in banks from Switzerland to Singapore, New Delhi is enforcing strict policies and tighter regulations to bring black money back to Indian shores. Meanwhile Since President Xi took over, Beijing has also come down heavily on evaders in a major clampdown on both government officials and businessmen.

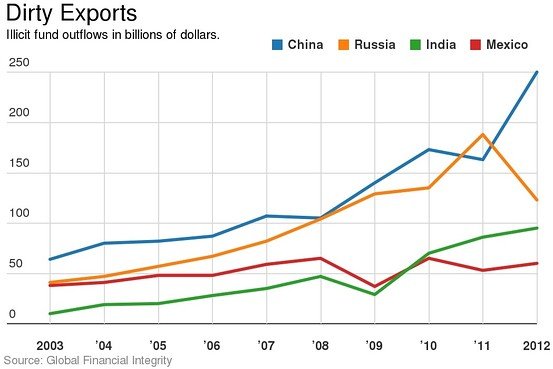

According to a report by Global Financial Integrity, Russia and China scale above India in the illicit funds that sit overseas. According to the report, India’s total (US$95 billion) is still less than 40 percent of China’s US$250 billion in illicit fund exports in 2012 but it’s gaining ground. Ten years earlier India’s total was only 20 percent of China’s, according to data from the Washington DC-based research and advocacy organization. Russia was on the top with US$123 billion in 2012.

According to Global Financial Integrity government officials and traders were the top culprits. For instance, a Chinese product with actual selling price of Rs 1,000on the mainland is imported with the invoice showing it as Rs 400 and the balance payment is made through the illegal route using the black money. The import duty is calculated on the basis of the invoice price and as such the exchequer is also the loser. Practiced only to avoid taxes, both India and China are recently in the process of signing treaties with several countries to help exchange information on stacks of cash aboard.